Optimize Your Credit Cards

Establishing good credit is the first step in building an infrastructure for getting rich.

- Our largest purchases are almost always made on credit, and people with good credit save tens of thousands of dollars on these purchases.

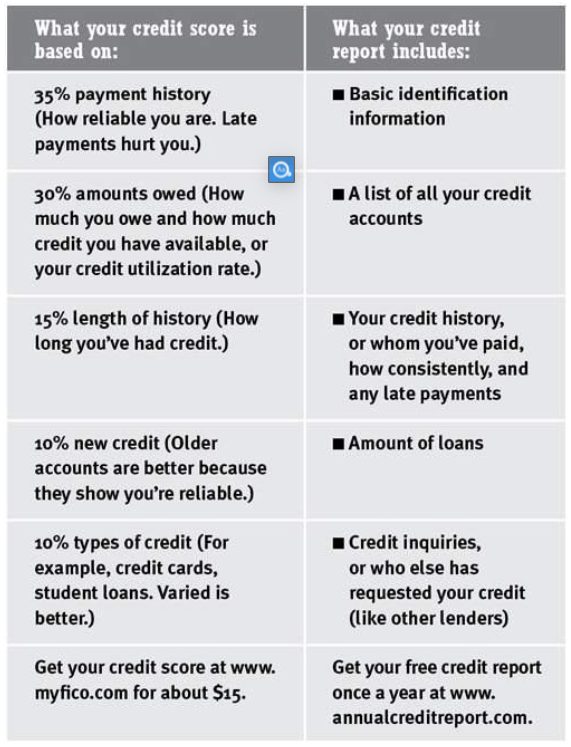

Credit Score Vs. Credit Report

Your credit report

- gives potential lenders—the people who are considering lending you money for a car or home—basic information about you, your accounts, and your payment history.

- tracks all credit-related activities, although recent activities are given higher weight.

Your credit score

- is a single, easy-to-read number between 300 and 850 that represents your credit risk to lenders.

- The lenders take this number (higher is better) and, with a few other pieces of information, such as your salary and age, decide if they’ll lend you money for credit like a credit card, mortgage, or car loan. They’ll charge you more or less for the loan, depending on the score, which signifies how risky you are.

Why are your credit report and credit score important?

Because a good credit score can save you hundreds of thousands of dollars in interest charges!

- If you have good credit, it makes you less risky to lenders, meaning they can offer you a better interest rate on loans

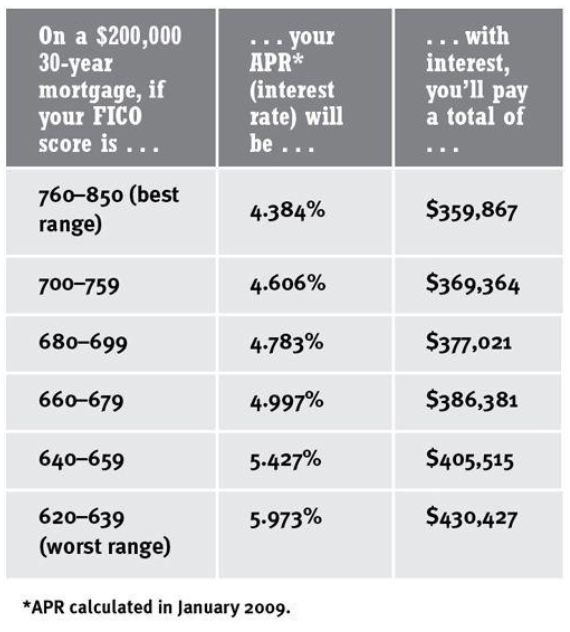

Example: Assuming you borrowed $200,000 for a 30-year mortgage, look at the differences in what you’d pay based on your credit score.

Building Credit with Credit Cards

One of the biggest problems with credit cards is the hidden cost of using them. Credit card charges are some of the largest unnecessary fees you’ll ever pay (although they are not obvious).

To get the most out of using credit, you need to optimize your credit card(s) and use them as a spearhead to improve your overall credit.

Getting a New Card

Avoid those credit card offers you receive in the mail.

- Taking a credit card offer you get in the mail is like marrying the first person who touches your arm—99 percent of the time it’s the easy decision, not the right one

Avoid cash-back cards, which don’t actually pay you much cash.

Compare cards online.

- The best way to find a card that is right for you is by researching different offers online

- In most cases, the simplest credit cards are offered by your bank

Rewards are important.

If you’re getting a rewards card, find one that gives you something you value.

Don’t go card crazy.

- There’s no magic number of cards you should have. But each additional card you get means added complexity for your personal-finance system.

- Good rule of thumb: two or three

The Six Commandments of Credit Cards

Pay off your credit card regularly.

The single most important thing you can do to improve your credit is to pay your bills on time.

Do NOT give your credit card company the opportunity to raise your rates and lower your credit score by being a few days late with your payment.

Get all fees waived on your card.

This is a great, easy way to optimize your credit cards because your credit card company will do all the work for you. Just call them using the phone number on the back of the card and ask if you’re paying any fees, including annual fees or service charges.

Negotiate a lower APR.

APR, or annual percentage rate, is the interest rate your credit card company charges you.

You want to avoid the black hole of credit card interest payments so you can earn money, not give it to the credit card companies. Call your credit card company and ask them to lower your APR.

- If they ask why, tell them you’ve been paying the full amount of your bill on time for the last few months, and you know there are a number of credit cards offering better rates than you’re currently getting.

Your APR doesn’t technically matter if you’re paying your bills in full every month.

Keep your cards for a long time and keep them active.

- Don’t get suckered by introductory offers and low APRs. If you’re happy with your card, keep it.

- If you’re getting a new credit card, don’t close the account on your old one. → That can negatively affect your credit score. As long as there are no fees, keep it open and use it occasionally. To avoid having your account shut down, set up an automatic payment on any card that is not your primary card.

Good practice: If you have a credit card, keep it active using an automatic payment at least once every three months.

Get more credit.

Warning: This tip is only for people who have no credit card debt and pay their bills in full each month. It’s not for anyone else.

It involves getting more credit to improve something called your credit utilization rate, which is simply how much you owe divided by your available credit. This makes up 30 percent of your credit score.

Example

If you owe $4,000 and have $4,000 in total available credit, your ratio is 100 percent (4,000 ÷ 4,000 × 100), which is bad. If, however, you owe only $1,000 but have $4,000 in available credit, your credit utilization rate is a much better 25 percent ($1,000 ÷ $4,000 × 100).

Lower credit utilization rate is preferred because lenders don’t want you regularly spending all the money you have available through credit—it’s too likely that you’ll default and not pay them anything.

Improve the credit utilization rate

- Stop carrying so much debt on your credit cards (even if you pay it off each month) or

- Increase your total available credit.

Use your rewards!

You can get great deals on your credit when you’re a responsible customer.

→ You should call your credit cards and lenders once per year to ask them what advantages you’re eligible for. Often, they can waive fees, extend credit, and give you private promotions that others don’t have access to.

Mistakes to Avoid

Avoid closing your accounts (usually).

- Although closing an account doesn’t technically harm your credit score, it means you then have less available credit —with the same amount of debt.

- People with zero debt get a free pass. If you have no debt, close as many accounts as you want. It won’t affect your credit utilization score.

Manage debt to avoid damaging your credit score.

Think ahead before closing accounts.

- If you’re applying for a major loan—for a car, home, or education—don’t close any accounts within six months of filing the loan application. You want as much credit as possible when you apply.

- However, if you know that an open account will entice you to spend, and you want to close your credit card to prevent that, you should do it. You may take a slight hit on your credit score, but over time, it will recover—and that’s better than overspending.

Don’t play the zero percent transfer game.

- You can make a few bucks a year, or maybe even a few hundred, but the waste of time, risk of mismanaging the process, and possibility of screwing up your credit score just aren’t worth it.

- Most important, this is a distraction that gets you only short-term results! You’re much better off building a personal-finance infrastructure that focuses on long-term growth, not on getting a few bucks here or there.

Avoid getting sucked in by “Apply Now and Save 10 Percent in Just Five Minutes!” offers.

- Stay away from these cards issued by every single retail store!

Don’t make the mistake of paying for your friends with your credit card and keeping the cash—and then spending it all.

Debt

When credit cards go bad

Just like with gaining weight, most people don’t get into serious credit card debt overnight. Instead, things go wrong little by little until they realize they’ve got a serious problem. The good news is that credit card debt is almost always manageable if you have a plan and take disciplined steps to reduce it. Yes, it’s hard, but you can get out of debt.

The key to using credit cards effectively is to pay off your credit card in full every month.

Pay your debt off aggressively

If you’ve found yourself in credit card debt—whether it’s a lot or a little—you have a triple whammy working against you:

- You’re paying tons of high interest on the balance you’re carrying.

- Your credit score suffers—30 percent of your credit score is based on how much debt you have—putting you into a downward spiral of trying to get credit to get a house, car, or apartment, and having to pay even more because of your poor credit.

- potentially most damaging, debt can affect you emotionally. It can overwhelm you, leading you to avoid opening your bills, causing more late payments and more debt, in a downward spiral of doom.

Make sacrifices to pay off your debt quickly. Otherwise, you’re costing yourself more and more every day.

If you set up automatic payments and work your debt down, you won’t pay fees anymore. You won’t pay finance charges. You’ll be free to grow your money by looking ahead.

Steps to ridding yourself of credit card debt

1. Figure out how much debt you have.

- You can’t make a plan to pay off your debt until you know exactly how much you owe. It might be painful to learn the truth, but you have to bite the bullet.

- Then you’ll see that it’s not hard to end this bad habit.

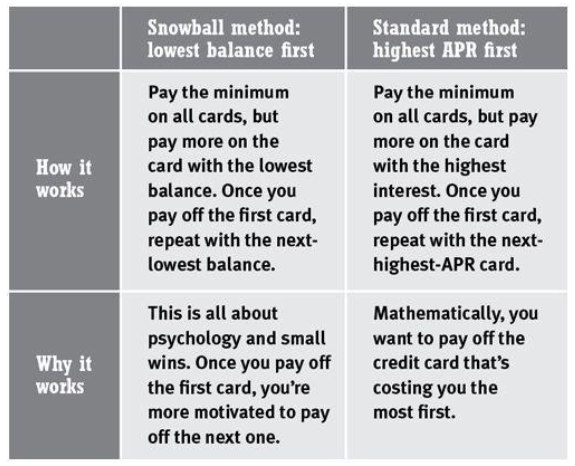

2. Decide what to pay off first.

- Standard method: you pay the minimums on all cards, but pay more money to the card with the highest APR, because it’s costing you the most.

- Dave Ramsey Snowball method: you pay the minimums on all cards, but pay more money to the card with the lowest balance first—the one that will allow you to pay it off first. (Not the most efficient approach, but on a psychological level, it’s enormously rewarding to see one credit card paid off, which in turn can motivate you to pay off others more quickly. )

Bottom line: Don’t spend more than five minutes deciding. Just pick one method and do it. 💪

3. Negotiate down the APR.

4. Decide where the money to pay off your credit cards will come from.

- Balance transfer is just a “Band-Aid” for a larger problem (usually your spending behavior). It is a confusing process fraught with tricks by credit card companies to trap you into paying more, and the people who do this usually end up spending more time researching the best balance transfers than actually paying their debt off.

- Better option: call and negotiate the APR down on your current accounts.

How to get Out of Your credit card debt in a right way

First, you need the cash flow.

You need to have enough income every month to meet your regular obligations like groceries, utilities, your mortgage, and the minimum payments on your credit cards, plus enough to throw toward putting that debt away for good.

If you do not have enough income to cover more than your minimum payments, you have to clear that hurdle by earning more money, negotiating with your credit card issuers to lower your minimum payments, or working with a legitimate, nonprofit debt consolidation organization that negotiates with creditors on your behalf, not one that provides you with a loan.

Next, prioritize your credit cards.

- List your debts from highest interest rate to lowest.

Pay the minimum on everything except the top card

- Once your credit cards are ranked properly, pay the minimum amount due listed on the statement for every card except the one at the top of the list. Dedicate all the extra funds you have to paying it off.

- Do this every month until that first credit card balance disappears. Then move to the second card on the list.

Stop using your cards.

Don’t cancel your cards, but stop using them.