ETFs and Taxes - Tax Aspects of Investing

💡Take Away

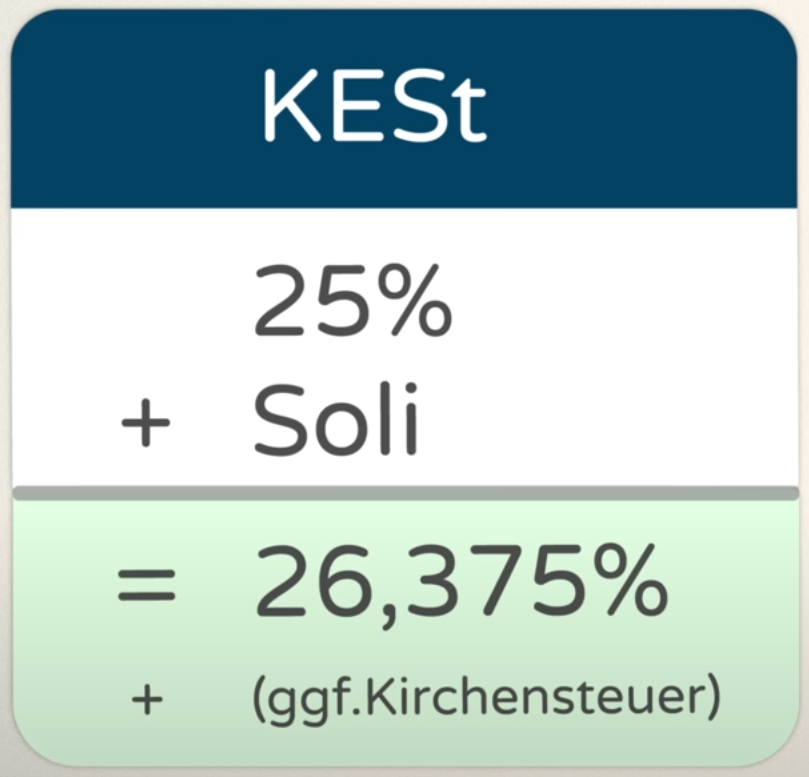

ETF earnings are subject to capital gains tax at a rate of 25%. In addition, there is a solidarity surcharge (5.5% on the tax) and possibly church tax.

Interest, dividends, and realized capital gains are taxed.

The capital gains tax is directly withheld by German custodial banks and remitted to the tax office.

The saver’s lump sum is your annual tax-free allowance and amounts to €1,000 or €2,000 for married couples per year. To directly apply this, a tax exemption order should be placed with the custodial account.

To align the taxation of distributing and accumulating ETFs, an advance lump sum may be applied. However, accumulating ETFs typically still provide a tax deferral effect.

For a joint custody account, gift tax may apply, so separate accounts are recommended.

Many investors are intimidated by dealing with the taxes due when it comes to ETFs and similar investments. However, the rules are relatively simple and should not discourage anyone from investing in ETFs, especially since they are automatically deducted by German custodial providers.

What taxes apply to ETF investments?

The taxes on ETF investments consist of three components:

- capital gains tax (25%)

- solidarity surcharge (5.5% of capital gain tax)

- possibly church tax (8% or 9%)

Capital Gains Tax 25%

The capital gains tax, also known as the flat-rate withholding tax, is currently set at a flat 25% 🤪.

- This rate does not change depending on the amount of taxable returns. It is a so-called withholding tax, meaning it is directly deducted at the source where the capital gains are generated, in this case, the depot or broker.

- For investors, this is advantageous because they are guaranteed to pay this tax without needing to worry about filing a tax return.

Solidarity Surcharge (Soli) 5.5%

The often criticized solidarity surcharge still applies to investors. Since 2021, around 90% of wage and income taxpayers no longer pay the solidarity surcharge. However, it remains for higher earners and corporations. The rate of the solidarity surcharge is 5.5% of 25%, which amounts to 1.375%.

Possible Church Tax of 8% or 9%

Those who are subject to church tax, as they are members of a religious community that collects this tax through the state, must pay an additional 8% (in Bavaria and Baden-Württemberg) or 9% (in all other federal states) on the capital gains tax owed. It is possible to apply for a blocking notice with the Federal Central Tax Office to prevent the religion affiliation from being passed on to the relevant banks, and thus avoid the automatic deduction of church tax.

What exactly are the taxes applied to in ETFs?

The capital gains tax is applied flatly to these three types of capital returns:

Interest: For example, interest earned from a fixed deposit account.

Dividends/Distributions: Such as dividends from dividend-paying stocks.

Realized Capital Gains: For instance, through a stock whose selling price is higher than its purchase price.

How to Effectiverly Save Tax?

Exemption for capital investments

As with many other tax models, there is also an exemption for capital gains tax. This is called the Saver’s Allowance (Sparerpauschbetrag).

The Saver’s Allowance is €1,000 for individuals and €2,000 for married couples per year. It is possible to split this amount across different financial institutions. The principle of cash inflow applies here. Taxes on capital gains exceeding the Saver’s Allowance are due when they are generated.

A tax exemption order can be set up by the end of the year. If someone forgets to submit such an exemption order, they can still reclaim the taxes via a tax return to the tax office. However, this takes unnecessary time and is much more complicated than simply setting up the exemption order in advance.

Additional tax advantage: The partial exemption rate for ETFs

In addition to the Saver’s Allowance, a portion of the investment volume has been tax-exempt since the Investment Tax Reform of 2018 and 2019. The amount that is exempt is determined by the so-called partial exemption rate (Teilfreistellungsquote). This applies to both distribution gains and the preliminary flat-rate tax.

The amount of the partial exemption rate depends on the composition of the fund. For example, if the equity share exceeds 50%, as in many equity ETFs, 30% of the distributions are tax-exempt.

| Fund Type | Composition | Partial Exemption Rate |

|---|---|---|

| Real Estate Funds | ≥51% Real Estate | 60% |

| Equity Funds | ≥51% Equity Share | 30% |

| Mixed Funds | ≥25% Equity Share | 15% |

| Mixed Funds | <25% Equity Share | 0% |

Note: the partial exemption rate does not apply to ETFs that synthetically replicate the capital market through swaps, known as fully funded swap ETFs. This is because the exemption only applies to actual capital investments in the market. However, fully funded swaps are relatively rare in the ETF market.

Low earners: Tax-free thanks to the non-assessment certificate

Since the capital gains tax is set at 25%, it may be higher than the personal marginal tax rate paid on income for certain groups such as students or low earners. To compensate for this, there is the option of obtaining a non-assessment certificate (also called NV certificate, Nichtveranlagungs-Bescheinigung). This can be applied for at the tax office. Those who have been issued such a certificate will have their earnings taxed at their personal marginal tax rate.

Preliminary Flat-rate and ETFs

Since the investment tax reform at the beginning of 2019, there has been a so-called preliminary flat rate (Vorabpauschale), which aims to restore the tax balance between accumulating and distributing funds or ETFs.

Previously, accumulating ETFs were highly advantageous because tax deductions were only made when the earnings were realized. -> This reduced the tax deferral effect, which occurs when tax payments are postponed until the gains are realized.

The preliminary flat rate seeks to balance this. It is limited by the fact that it only applies if it is lower than the capital appreciation of the fund for which it is calculated. This means that no preliminary flat rate is charged for ETFs without capital appreciation or even with losses.

The preliminary flat rate is the basis for the taxation of, especially, accumulating ETFs. It is calculated from the capital appreciation of the fund, a share of the Bundesbank base interest rate, and the respective partial exemption according to the type of fund.

It can be easily calculated with the preliminary flat rate calculator.

Which is Better for Taxes: Distributing or Accumulating?

For the preliminary flat rate, a fictional capital appreciation is assumed.

- The Deutsche Bundesbank sets a base interest rate for this. During the low-interest phase, the base interest rate was negative, so no preliminary flat rate was applied.

- E.g., for the year 2023, the base interest rate was 2.55%. If you made capital gains with your funds in the previous year, a preliminary flat rate will apply in 2024.

The preliminary flat rate is generally lower than the tax on distributions.

- It is also possible that a preliminary flat rate will be charged in addition to the distributions for a distributing fund.

- However, the tax burden on an accumulating fund is at most as high as that of the distributing fund. This is why the deferral effect usually applies to the distributing fund. This is very attractive for long-term investors.

The saver’s allowance (Sparerpauschbetrag) provides opportunities for investors to save on taxes. Both methods take advantage of the saver’s allowance, as tax-free fund income is not taxed again—such as during the final sale. Therefore, it makes sense to fully utilize the saver’s allowance, for example, by using distributing ETFs.

- Many brokers offer automatic reinvestment, allowing the distributing ETF to cover its income with the saver’s allowance while still providing the compound interest effect of an accumulating ETF.

- Alternatively, sales can also be made with an accumulating ETF. In this case, just enough shares are sold to fully utilize the saver’s allowance.

Avoiding Gift Tax with ETF Accounts

For (married) couples, the question arises whether to open a joint account or two individual accounts. Since gift tax may come into play with a joint account, the clear recommendation is to always open two separate accounts.

Explanation

The sensible approach is to open two separate accounts and, if necessary, grant each other powers of attorney. This way, partners can access each other’s accounts, but the gift tax exemption remains untouched.

Summary

- The capital gains tax is 25%, plus an additional 1.375% solidarity surcharge (Soli) and possibly church tax. It is applied to interest, dividends, and realized capital gains.

- As a withholding tax, the capital gains tax is directly deducted at the source, i.e., by the account provider. Therefore, you should set up an exemption order (Freistellungsauftrag) to make use of the tax-free allowance, known as the saver’s allowance (Sparerpauschbetrag), which is €1,000 for individuals or €2,000 for married couples.

- The preliminary flat rate (Vorabpauschale) is mainly applicable to accumulating ETFs. However, accumulating ETFs often provide a tax deferral effect for investors.

- To save taxes, it is advisable to fully utilize the saver’s allowance – this can be done with distributing ETFs, through the preliminary flat rate, or by making sales.